Deductible vs Out-of-Pocket Maximums

Introduction

People often wonder what the difference is between a deductible and an out-of-pocket (OOP) maximum. So what’s the difference, you ask? The deductible is the amount you must meet before your insurance starts paying for your medical expenses. After that, the plan usually switches to coinsurance, where you share costs with your insurance.

The out-of-pocket maximum, on the other hand, is the cap on what you’ll spend in a year. It includes your deductible, copays, and coinsurance. Once you hit it, your insurance pays 100% of covered expenses for the rest of the year.

By the end of this article, you’ll know how these two numbers work together and how to budget for your healthcare costs more effectively. Let’s begin.

What Is a Deductible?

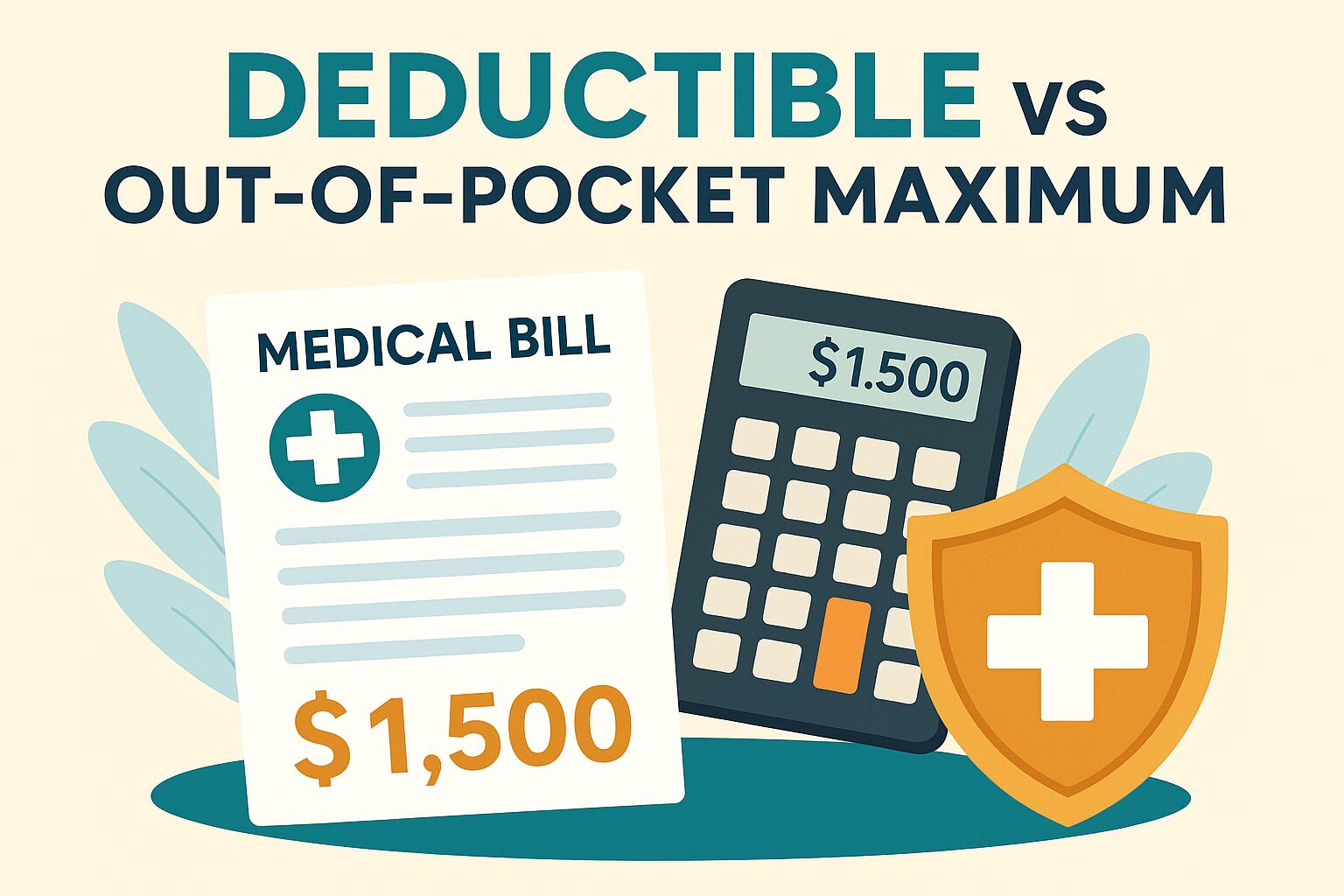

The deductible is the amount you must pay in full before your health insurance begins sharing costs.

For example, if your plan has a $1,500 deductible, you must cover $1,500 in medical expenses out of pocket before insurance contributes. This can happen across multiple visits—doctor appointments, specialist visits, ER trips, physical therapy, diagnostic tests, etc.

Note: Preventive care and annual wellness visits are typically covered before the deductible under most ACA-compliant plans.

What Is an Out-of-Pocket Maximum?

The out-of-pocket maximum (OOP max) is the annual cap on what you’ll spend for covered services.

For example, if your OOP max is $8,000, once you’ve paid $8,000 in deductibles, copays, and coinsurance, your insurance covers 100% of additional covered costs for the rest of the plan year.

You can read more about how the government defines out-of-pocket maximums at Healthcare.gov.

This resets at the beginning of each new policy year.

Deductible vs Out-of-Pocket Maximum (Side-by-Side)

Here’s how they compare:

| Feature | Deductible | Out-of-Pocket Maximum |

| Definition | What you pay before insurance starts sharing costs | The total you’ll pay in a year for covered services |

| Includes | Medical costs you pay directly before coinsurance applies | Deductible + copays + coinsurance |

| Resets | Every plan year | Every plan year |

| Example | $1,500 | $8,000 |

| After Met | Insurance begins paying its share (usually coinsurance) | Insurance pays 100% of covered costs |

Timeline of Spending:

- You pay 100% of medical costs until deductible is met.

- Then, you share costs with coinsurance/copays.

- Once total spending hits the OOP max, insurance covers everything else for the year.

Why These Numbers Matter in Choosing a Plan

The type of healthcare coverage you choose can make a huge difference:

- High-deductible plans often allow you to open a Health Savings Account (HSA), which lets you save pre-tax dollars to cover future healthcare.

- Low-deductible plans may only offer a Flexible Spending Account (FSA), which has “use-it-or-lose-it” rules.

- If you’re healthy with few medical expenses, a high-deductible plan + HSA can help you save and grow funds tax-free.

- If you have chronic conditions, a lower deductible may help you avoid steep upfront costs.

Either way, the OOP max acts as a safety net to protect you from financial catastrophe during a bad health year.

For details on how HSAs work and current contribution limits, see the IRS guide on HSAs.

Smart Strategies to Manage Costs

Here are a few ways to stay ahead of healthcare costs:

- Use HSAs or FSAs strategically depending on your plan.

- Keep track of what’s already been applied to your deductible and OOP max (many insurers provide a tracker in your online account).

- Review your coverage each open enrollment period to ensure you’re in the best plan for your health and finances.

Conclusion

The deductible is the threshold you pay first, while the OOP max is your financial safety net for the year. Together, they define your maximum exposure to healthcare costs.

When shopping for insurance, balance your healthcare needs, tax-advantaged accounts, and ability to cover the deductible or OOP max in case of a medical emergency.

👉 Take a moment to check your insurance portal today—you may be closer to hitting your deductible or OOP max than you think.

To explore this concept further, visit our main tax and insurance page.

Question for You:

What’s the most confusing part about deductibles and out-of-pocket maximums for you? Drop a comment below—I’d be happy to help clear things up.