Health Insurance Basics: Understanding Your Coverage

Let’s face it—healthcare in the United States is expensive. Hospitals often charge high rates to cover operating costs, drug companies mark up brand-name medications, and one unexpected illness or accident can leave you facing overwhelming bills. Without insurance, many families are just one emergency away from financial ruin.

That’s why health insurance is essential. It protects you from catastrophic costs, gives you access to care, and offers peace of mind. The challenge is that the terminology—deductibles, coinsurance, networks—can feel like a foreign language.

Here’s the good news: by the end of this guide, you’ll understand the core terms, types of plans, and how to choose coverage that fits your needs and budget. Let’s break down the basics.

Why Health Insurance Matters

- Financial protection: A single hospital stay could cost tens of thousands of dollars. Insurance shields you from paying it all out of pocket.

- Preventive care: Many plans cover annual checkups, screenings, and certain prescriptions at little or no cost, helping you avoid costly long-term health issues.

- Peace of mind: Whether it’s a broken leg or a major health event, insurance ensures you won’t go bankrupt because of medical bills.

Key Health Insurance Terms

- Premiums: The monthly payment you make to keep your policy active.

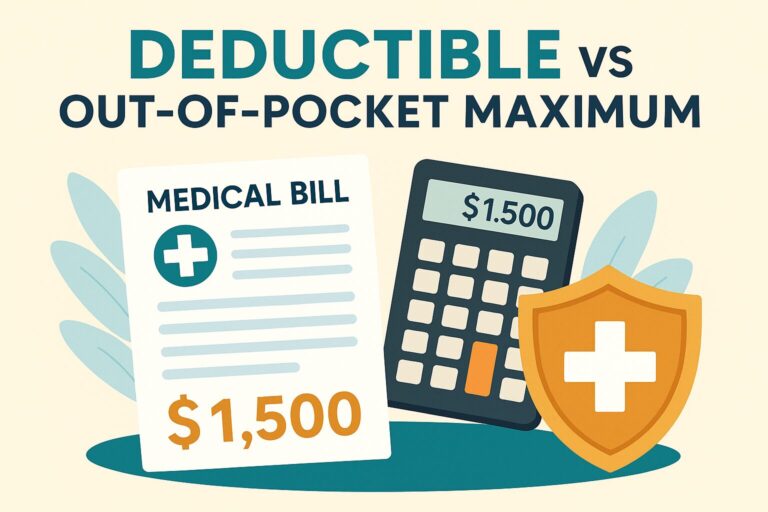

- Deductible: The amount you must pay out-of-pocket before your insurance begins sharing costs.

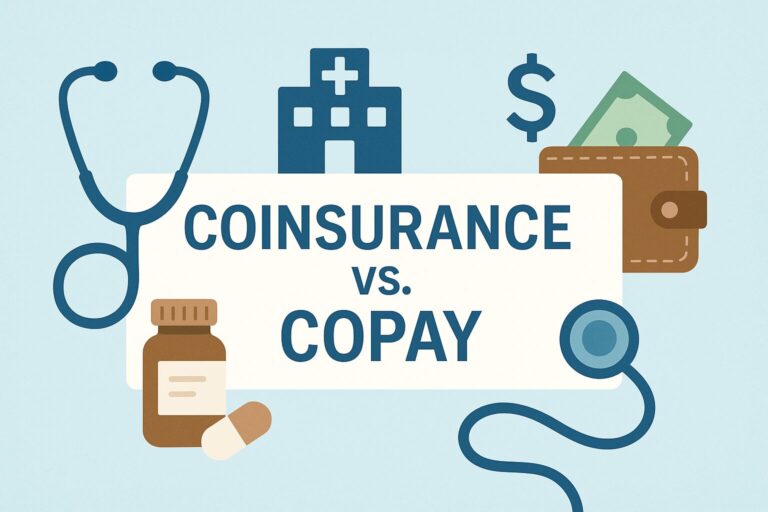

- Copayment (Copay): A fixed fee you pay at the time of service (e.g., $35 for a doctor’s visit).

- Coinsurance: Instead of a flat fee, you pay a percentage of the cost—commonly 20% while the insurer pays 80%.

- Out-of-pocket maximum: The most you’ll pay in a year for covered care. Once you hit this limit, your insurance covers 100%.

- Network: “In-network” providers have contracts with your insurer, lowering your costs. “Out-of-network” providers may cost much more or not be covered at all.

Types of Health Insurance Plans

- Employer-sponsored plans: Offered through your job, often with employer contributions toward premiums.

- Marketplace/ACA plans: Available at HealthCare.gov or state exchanges. Subsidies may lower costs, but overestimating subsidies could lead to higher taxes later.

- Medicare and Medicaid: Government programs. Medicaid covers low-income individuals and families. Medicare covers all citizens 65+ and some with disabilities.

- Short-term or catastrophic plans: Lower-cost options that cover only major emergencies. They don’t work well if you have ongoing medical needs or prescriptions.

Choosing the Right Plan

When evaluating health insurance, consider:

- Cost: Balance the premium with deductibles and out-of-pocket expenses.

- Coverage: Are your needs simple, or do you require broader coverage?

- Network: Check if your current doctors and preferred hospitals are in-network.

- Prescriptions: Make sure your medications are covered and review their copay tiers.

You’ll also want to compare high-deductible vs. low-deductible plans:

- Low-deductible plans (<$1,000) often have higher premiums but predictable copays.

- High-deductible plans lower premiums but require more out-of-pocket spending upfront until coverage kicks in.

Tax-advantaged accounts can also help:

- Health Savings Account (HSA): Save tax-free for medical costs, and funds roll over year to year. Available with high-deductible plans.

- Flexible Spending Account (FSA): Lets you set aside pre-tax money for medical costs, but most funds must be used within the year. Some employers allow limited rollover.

Common Mistakes to Avoid

- Choosing only by lowest premium: Cheap plans often come with high deductibles or limited coverage.

- Ignoring the network: You may end up paying more—or switching doctors—if your providers aren’t covered.

- Skipping open enrollment reviews: Plans change yearly. Always re-check options to ensure you’re getting the best fit for your needs.

Conclusion

Health insurance is one of the most important financial protections you can have. Get it wrong, and you risk bankruptcy from unexpected medical costs. Get it right, and you’ll have security, access to care, and peace of mind.

Now that you understand the basics, take time to review your current policy. Does it meet your needs? Could you save money—or gain better coverage—by switching?

What part of health insurance is most confusing to you? Did this article help clear things up? Share your thoughts—I’d be glad to help make sense of the insurance maze.

To explore this concept further, visit our main taxes and insurance page.